Do Lower Fed Rates Mean Soaring Home Prices? A Data-Driven Analysis (2000–2025)

Published | Posted by Dan Price

Will Home Prices Soar When the Fed Lowers Rates? A Historical Analysis

When the Federal Reserve lowers the federal funds rate, many assume mortgage rates will follow, leading to a rapid recovery—or even a boom—in home prices. It’s a common narrative in housing market discussions, but historical data reveals a far more nuanced reality. By examining inflation-adjusted home prices through the Home Price Index (HPI) relative to the Consumer Price Index (CPI), alongside Freddie Mac’s Primary Mortgage Market Survey rates from 2000 to April 2025, we can better understand how changes to the federal funds rate, mortgage rates, and home prices actually interact. This analysis provides insight into whether lower Fed rates reliably trigger soaring home prices—or whether the story is more complex.

The Relationship Between Fed Policy, Mortgage Rates, and Home Prices

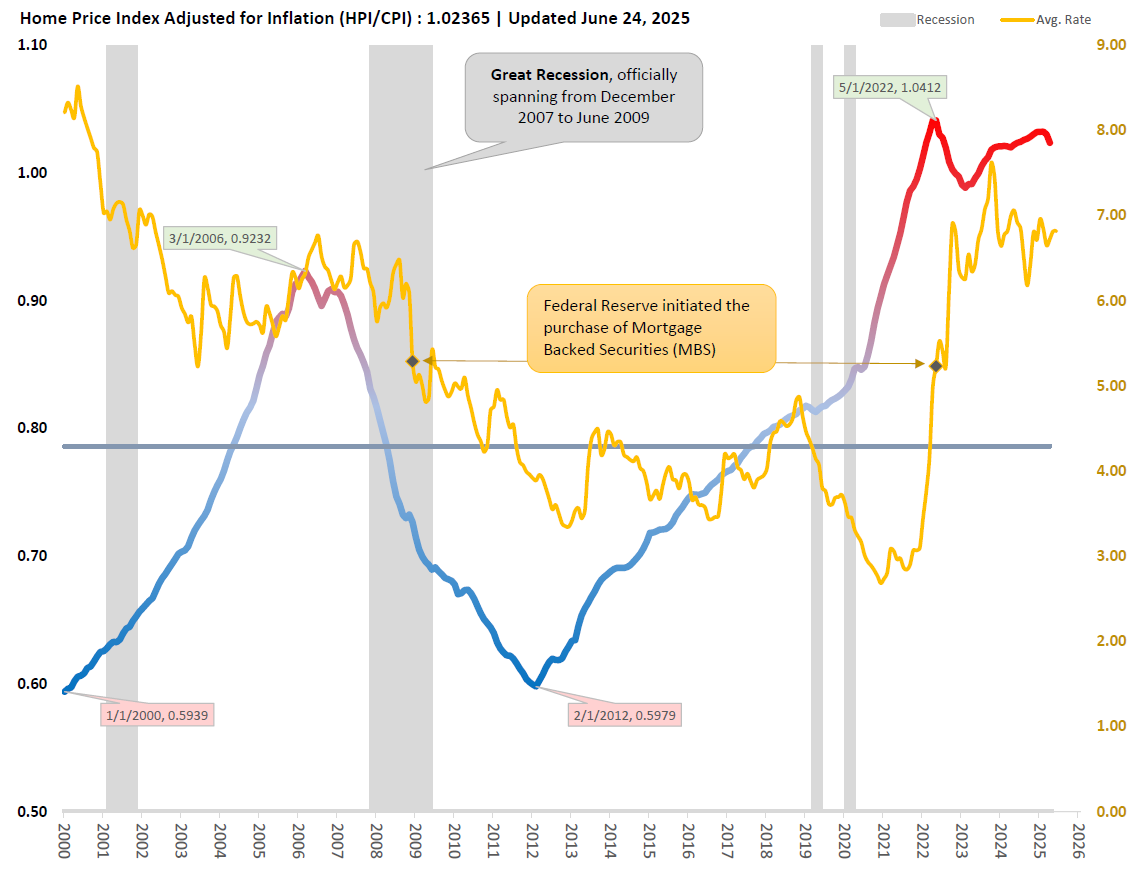

The federal funds rate is the interest rate at which banks lend to one another overnight. While this short-term rate indirectly influences longer-term borrowing costs, including mortgage rates, its impact depends heavily on broader market dynamics like investor confidence, inflation expectations, and overall economic conditions. For example, following the dot-com bubble and 9/11 attacks, the Fed aggressively reduced the federal funds rate from 6.5% in 2000 to 1.25% by late 2002. Mortgage rates fell accordingly, declining from 7.38% to 6.05%. During that same period, the inflation-adjusted HPI/CPI rose from 0.6251 to 0.7020, marking a 12.31% increase. While home prices grew steadily, this period did not produce a dramatic surge in prices, illustrating that lower rates supported the market but didn’t fuel runaway appreciation.

The 2008 Financial Crisis: A Case Study in Market Complexity

The period following the 2008 financial crisis offers perhaps the most instructive example of how lower rates and housing markets interact. In response to the crisis, the Fed slashed the federal funds rate to near zero and, for the first time, launched large-scale purchases of Mortgage-Backed Securities (MBS) in December 2008. At that time, the HPI/CPI stood at 0.7267, while mortgage rates hovered at 5.29%. The Fed’s intervention eventually pushed mortgage rates down to 3.89% by February 2012. Yet, despite these aggressive rate cuts and targeted efforts to stimulate lending, home prices continued to decline for over three years.

From the March 2006 market peak, when the HPI/CPI was 0.9232 and mortgage rates were 6.32%, to the February 2012 bottom, home prices dropped a staggering 35.23%. Even after the Fed’s intervention began, prices fell an additional 17.72% over 38 months. This period makes it clear that lower rates alone cannot override deeper macroeconomic challenges like high unemployment, foreclosures, and weakened demand.

Gradual Recovery, Not Rapid Rebound

Following the February 2012 bottom, the housing market began a slow, methodical recovery. By December 2013, the HPI/CPI had climbed to 0.6859, a 14.74% increase from the low point. Mortgage rates during this recovery fluctuated between 3.35% and 4.46%. Yet, even with these historically low rates, the market required years to regain its pre-crisis levels. The path to recovery was anything but immediate. This illustrates an important reality for today’s market observers: lower rates can create favorable conditions for price growth, but they don’t automatically lead to sharp or sudden price surges.

Federal Funds Rate Cuts vs. MBS Purchases: What Really Moves the Needle?

Historical comparisons further demonstrate the distinction between standard federal funds rate cuts and more aggressive, targeted interventions like MBS purchases. Between 2001 and 2003, the Fed reduced the federal funds rate substantially, and mortgage rates followed suit—dropping from 7.07% to 5.88%. During that same window, inflation-adjusted home prices increased moderately, with the HPI/CPI rising from 0.6564 to 0.7557—a 15.13% gain. In contrast, the 2008–2012 period saw the Fed deploy both near-zero interest rates and unprecedented MBS purchases. Mortgage rates fell sharply, yet prices still declined for years before stabilizing. This underscores that while lower borrowing costs are important, other factors—such as job security, consumer sentiment, inventory levels, and foreclosure rates—play equally significant roles in determining home price trends.

Recent Trends: 2022 to 2025

Fast-forward to the present, and we see another period of shifting monetary policy and market dynamics. The inflation-adjusted HPI/CPI peaked at 1.0412 in May 2022, with mortgage rates at 5.23%. As the Fed raised the federal funds rate aggressively to combat inflation, mortgage rates climbed to 7.62% by October 2023. Predictably, home prices responded, with the HPI/CPI declining to 1.0182, a 2.21% drop. By April 2025, mortgage rates had moderated to 6.73%, and home prices had stabilized, with the HPI/CPI at 1.0237. This modest recovery occurred despite elevated borrowing costs, largely due to constrained inventory levels.

Looking ahead, if the Fed lowers rates in 2025, history suggests we could see mortgage rates fall moderately. However, any meaningful or rapid home price appreciation will still depend on broader factors like buyer demand, available housing supply, and economic stability—rather than rate cuts alone.

Conclusion: Rate Cuts Are Only Part of the Equation

The historical record is clear: while lower federal funds rates can support housing market stability, they do not guarantee soaring home prices. Mortgage rates are influenced by a web of factors, including Treasury yields, market expectations, and global economic conditions. Home prices, in turn, are driven by supply, demand, and the overall health of the economy. The Fed’s 2008–2012 MBS purchases successfully pushed mortgage rates to record lows, yet prices still fell significantly. Even during milder downturns, like the early 2000s, price growth was gradual, not explosive. Expecting a Fed rate cut alone to fuel immediate home price surges overlooks the complexity of these market dynamics.

FAQ Section:

How does the Federal Reserve lowering the federal funds rate affect mortgage rates?

The federal funds rate is the short-term interest rate at which banks lend to one another overnight. When the Fed lowers this rate, borrowing costs across the economy generally decline, which can lead to lower yields on Treasury securities—the benchmark for mortgage rates. However, the relationship is not always one-to-one. Historical examples, such as the 2000–2002 period, show that while federal funds rate cuts contributed to a decline in mortgage rates from 7.38% to 6.05%, the effect was modest compared to targeted actions like the Fed’s Mortgage-Backed Securities purchases, which drove rates down more dramatically from 5.29% to 3.89% between 2008 and 2012.

Why don’t home prices always rise when mortgage rates drop?

Home prices depend on more than just borrowing costs. Factors such as employment rates, consumer confidence, housing inventory, and overall economic conditions play major roles. Even significant mortgage rate reductions, like those seen from 2008 to 2012, failed to prevent a 17.72% price drop during the Great Recession. Similarly, low mortgage rates during the early 2000s supported moderate price growth, but did not produce a housing boom on their own.

What happened to home prices during the 2008 financial crisis?

Home prices saw a dramatic decline during the 2008 financial crisis. From a peak HPI/CPI of 0.9232 in March 2006, prices fell 35.23% over the next six years, bottoming out at 0.5979 in February 2012. Despite aggressive Fed interventions—including rate cuts and large-scale MBS purchases—high unemployment, foreclosures, and weakened demand prolonged the downturn.

How long does it take for home prices to recover after a market crash?

The recovery timeline depends on the severity of the downturn and broader economic conditions. After the 2008 crash, home prices bottomed in February 2012 and had recovered 14.74% by December 2013. However, it took several more years to return to pre-crisis price levels. In contrast, the milder 2022–2023 correction saw a modest 2.21% price decline and relative stabilization by April 2025, largely due to constrained housing supply.

What is the difference between the federal funds rate and mortgage rates?

The federal funds rate is a short-term rate controlled by the Federal Reserve to influence monetary policy. Mortgage rates, in contrast, are long-term rates primarily driven by the 10-year Treasury yield, market conditions, and investor demand for Mortgage-Backed Securities. While the Fed’s rate decisions can influence mortgage rates indirectly, factors such as inflation expectations and global economic stability often play larger roles.

Related Articles

Keep reading other bits of knowledge from our team.

Request Info

Have a question about this article or want to learn more?